Tag

health insurance

-

Stories to cover as Americans seek affordable health insurance

Following the expiration of Affordable Care Act tax credits on Dec. 31, many Americans are struggling to pay for health…

-

What freelancers should know about the impending health insurance premium hikes

In a Q&A, an expert shares what is likely changing for many self-employed people who buy health insurance through the…

-

Magazine editor shares how he got access to health insurer’s darkest secrets

Learn how New York Magazine editor Chris Stanton got insider info from four former health insurance executives.

-

Freelancers: Finding health insurance doesn’t have to be so difficult

As the number of staff jobs in journalism shrinks, many reporters are turning to freelancing and need a new health…

-

How to cover the case that could kill patients’ access to no-cost preventive services

A key provision of the Affordable Care Act is in jeopardy in the case of Braidwood Management Inc. v. Becerra…

-

History shows Inflation Reduction Act subsidies help Americans save on health insurance

By signing the Inflation Reduction Act (IRA) on Tuesday, August 16, President Biden made history by continuing a 12-year trend…

-

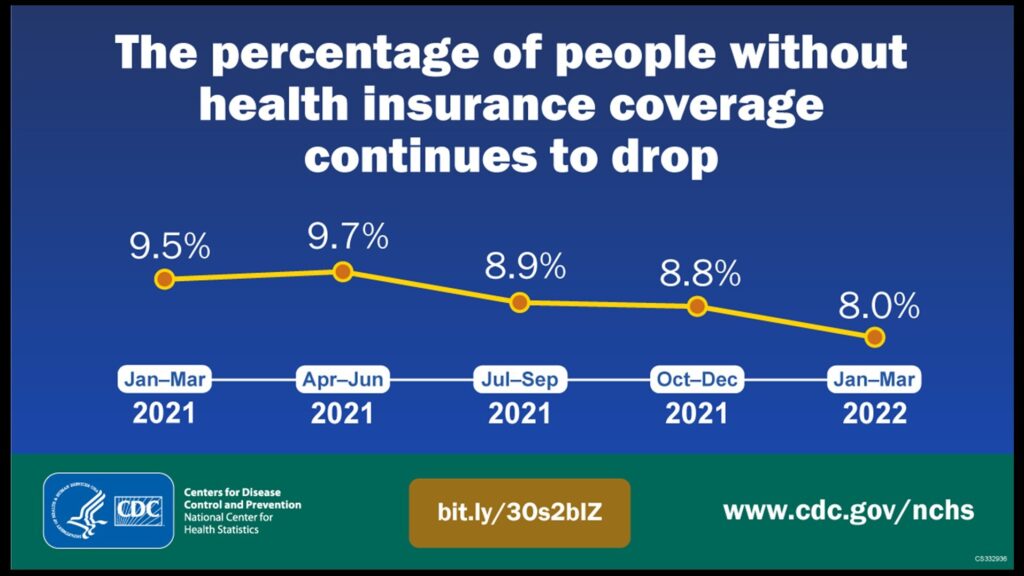

3 reasons it’s significant that the percentage of uninsured Americans hit an all-time low

The percentage of Americans who lack health insurance hit an all-time low of 8% in the first quarter of this…

-

ACA hits open-enrollment record, but swift action is needed to prevent rate hikes next year

After a record number of consumers signed up for health insurance coverage under the Affordable Care Act (ACA), Bob Herman…

-

Approximately 80% of consumers expected to save significantly on 2022 Affordable Care Act plans

Health insurance premiums will cost $10 or less each month next year for four out of five consumers shopping for…

-

Growing beyond the pilot stage, bundled payment gains wider acceptance

Health insurers are expanding the use of bundled payment as a core part of their efforts to reform how they…